A guide to KiwiSaver for kids

There are many reasons parents explore KiwiSaver for their children, including helping to grow their savings and teaching them good financial habits. However, there are a few key considerations to make when signing your kids up for KiwiSaver and some aspects that will differ until they are 18. Read our guide to make sure you understand how it all works before signing them up!

Joining KiwiSaver

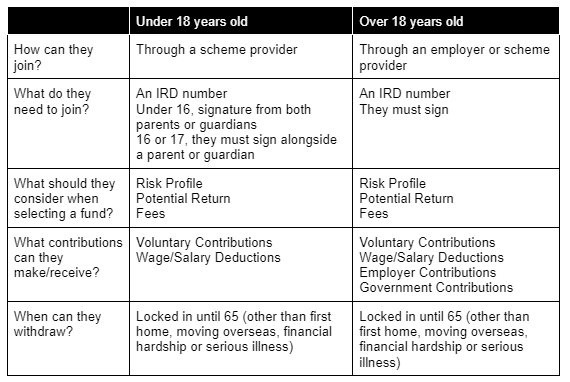

When signing your kids up for KiwiSaver, unlike over 18s, they can’t join through their employer even if they are working. They will need to join through a scheme provider and apply directly to them.

To apply, you’ll need their IRD number. If your child is under 16, both parents or guardians will need to sign the application form on their behalf. If your child is 16 or 17, they must sign the form alongside at least 1 parent or guardian.

Before signing your child up, consider the decision carefully as there is no option to opt-out even once they turn 18!

Selecting a fund

When signing your child up to KiwiSaver you’ll need to select a fund with your chosen provider to invest in. A Haven adviser can guide you through suitable options so you can consider carefully what fund is the best choice for your child currently. They will have the option to move funds again in the future.

Alongside considerations like risk and potential returns, you should look at the fees associated with a particular fund. As under 18s aren’t entitled to employer or government contributions, you don’t want your contributions to be eaten away by high fees.

Making contributions

For under 18s, the main way to contribute is through voluntary contributions. However if your child is working they will need to contribute a minimum of 3% of their wages or salary. Once they’ve been a member for 12 months they will have the option to take a savings suspension for 3 to 12 months.

Unlike over 18s, even if your child is working, their employer is not required to contribute. They also don’t qualify for the government contribution until they are 18.

Withdrawing

When you can withdraw your KiwiSaver is the same for all members. Generally, your money is locked away until you’re 65. However you may be able to withdraw funds to help buy your first home, if you’re permanently moving overseas, experiencing financial hardship or are seriously ill.

Summary

How can a Haven Financial Adviser help?

Our advisers are able to work with to help you decide which KiwiSaver fund is right for your child’s financial future. If you have any other questions, don’t hesitate to get in touch with our team.

5 ways to make the most of KiwiSaver when living costs are rising

The cost of living is hitting New Zealanders in the pocket, with interest rates and the price of everyday expenses continuing to rise. So for many, saving for retirement seems unrealistic, especially if retirement feels like a long way off.

However, contributing to KiwiSaver over the long term is important to ensure you’re able to grow your retirement savings over time. Even when times are tough it’s important to ensure you’re making the most of KiwiSaver in order to reach your long term savings goals.

Here are 5 ways to start making the most of KiwiSaver when the cost of living is increasing:

1. Check you’re contributing enough

Contributing enough to get the government contribution is one of the best ways to make the most of KiwiSaver and grow your savings.

If you’re eligible and contribute at least $1,042.86 of your own money between 1 July to 30 June each year you’ll receive the full government contribution of $521.43. To ensure you’ve contributed enough, check ahead of 1 July 2023, and you can make a voluntary contribution through the IRD or your provider.

2. Choose a fund that suits your needs

If you were automatically enrolled in KiwiSaver through your employer and never actively chose which fund to be in, it’s likely you’re in a default scheme which is typically conservative with lower potential returns. However to make the most of KiwiSaver it’s important to consider your fund and the associated potential investment returns.

KiwiSaver schemes have a variety of funds with different amounts of risk and differing potential returns. A Haven Adviser can help you ensure you’re in the most appropriate fund for your life stage and risk profile with potential returns that align with your expectations.

3. Keep an eye on your fees

All KiwiSaver funds charge fees, but some are more expensive than others. When money is already tight it’s important to make sure you’re aware of the fees associated with a fund and consider switching to a lower-cost option if necessary. Get in touch with a Haven Adviser to chat through your options.

4. Have a plan for your retirement

KiwiSaver is designed to help fund your retirement, so it’s important to think about how much you’ll need to live on in the future. Especially when the cost of living is rising, you may need more than you originally thought. You can use our online tool to see what your projected savings could look like based on your rate of contribution.

5. Stay informed

Keep up-to-date with the latest news and changes in KiwiSaver legislation. This’ll help you make informed decisions about KiwiSaver.

So how can a Haven Financial Adviser help?

Making the most of KiwiSaver doesn’t have to be DIY. Like any investment, doing your research and seeking financial advice can help you make the most of KiwiSaver, even during the cost of living crisis.

If you’ve never sat down with us to make a plan for your retirement savings, a Haven Financial Adviser can help you take into account the current constraints on your household budget and help you make a plan for the future. Get in touch today to get on the right track to make the most of KiwiSaver.

Take control of your KiwiSaver in 2023

Take a look at what fund you’re in

If you were automatically enrolled in KiwiSaver through your employer and never actively chose which fund to be in, it’s likely you’re in a default scheme which is more conservative and might not grow as much as you’d like come retirement.

There are a few different types of funds available, so you’ll need to do a bit of research and figure out how much risk you’re willing to take and how long your money will be in that fund (i.e. if you’re likely to be withdrawing some of your KiwiSaver for a first home soon, you might want to be in a lower risk fund).

Check out your contributions

If you’re enrolled in KiwiSaver, you’ll be contributing 3%, 4%, 6%, 8%, or 10% from your salary. If you began at the lower end of the scale but have since received a pay rise, you could look at contributing more to boost your KiwiSaver. Even increasing a 3% contribution to 4% might make a healthy difference to your balance over the long run.

If you’d like to see how much more you can add to your KiwiSaver by increasing your contribution rate, check out our handy calculator.

What fees are you paying?

Because KiwiSaver is an investment, KiwiSaver providers charge different fees for managing your account. If you’re getting great returns you might be happy to pay more in fees, but it’s a good idea to check out what fees you’re paying because there may be a better option out there for you.

If you’re not sure what fees you’re paying, Sorted has a great tool called Fund Finder to help you compare.

Can you withdraw your KiwiSaver funds early?

When can you withdraw your KiwiSaver funds?

You’re buying your first home

KiwiSaver can be a great (and often necessary) means of helping you get into your first home but it’s important to remember that it’s first and foremost for your retirement.

Make sure you consider all aspects of withdrawing for a first home, including how much you’d like to have when you retire, how much of it you need now for your first home, and how much you will keep contributing to it.

There are a few things to keep in mind when withdrawing from your KiwiSaver fund for a first home deposit:

- You’ll need a lawyer to receive your KiwiSaver fund and transfer it on your behalf before the settlement date

- You’ll need to notify your provider, they need proof of identity, a copy of the sale and purchase agreement and a letter from your lawyer

- You need to leave $1,000 left in your KiwiSaver account

You’re experiencing financial hardship

If you’re experiencing significant hardship, you might be able to withdraw some of your savings. However, the criteria is very strict and should be considered a last resort.

Your provider will require solid proof of your hardship such as bank statements, payslips, expenses and any demands made against you (eviction notices). It takes time for your provider to consider and it may take weeks, even then they might still say no.

You might be eligible if:

- You can’t meet minimum living expenses

- You can’t afford your mortgage repayments and your provder is taking action against you

- You can’t afford the cost of medical treatment for you or a dependent for a serious illness or injury

- You need to pay for a funeral of a deceased family member.

If your provider grants your request, they might not give you access to all of your KiwiSaver money, only enough to alleviate the hardship.

If you think your hardship is only temporary you can apply to suspend your contributions, that way it’s frozen and ready to grow once you’re back on your feet.

You’re leaving New Zealand

You can apply to withdraw your KiwiSaver fund if you have lived overseas for one year, unless you have been in Australia. If you’ve emigrated to Australia, you can transfer your funds to an Australian superannuation scheme.

If you’ve moved anywhere else in the world, you can withdraw your KiwiSaver funds by submitting an application. It must include proof of evidence such as permanent residency, letters from employers, rental or sale agreements and bank statements.

Get in touch with our friendly team today to talk about your KiwiSaver!

KiwiSaver Jargon made simple

Contributions

- Contribution – The money that is put into your KiwiSaver fund to invest. This can be from you, your employer or the government.

- Member contribution – Quite simply, this is what you are contributing to your KiwiSaver account.

- Employer contribution – This is the amount (after tax) that your employer contributes to your KiwiSaver account if you are employed. Your employer pays a minimum of 3% before tax.

- Savings suspension – Previously called a contributions holiday, this temporary stop to your KiwiSaver contributions is now called a suspension. You can suspend your KiwiSaver contributions for 3 months to a year if you’ve been contributing for at least 12 months. If you need to extend this period, you’ll need to reapply again for a savings suspension. Stopping your contributions means that you also won’t receive your employer or government contributions.

Funds

- Fund – A fund is a pool of money from many people that a fund manager invests. Each KiwiSaver scheme has a number of funds within it to choose from. There are also different types of funds, including conservative, balanced, growth, and aggressive.

- Default fund – A fund for KiwiSaver members who haven’t chosen which KiwiSaver scheme they’d like to be a part of. Default funds are typically conservative and low cost. To make the most of your KiwiSaver, default funds should only be used as a temporary solution until you’ve chosen the fund that’s best for you and your situation.

- Conservative – Conservative funds tend to have a lower-risk, lower-return model. There will still be ups and downs because KiwiSaver is an investment, but overall you’ll likely see less dramatic changes with this fund.

- Balanced – Balanced funds carry a little more risk, but you’ll usually get a little more return with this one too. This is considered a fairly steady fund.

- Growth – With a Growth fund, again you’ll see perhaps a higher risk, but also higher returns. You might see a few more ups and downs, but if you don’t plan to use your KiwiSaver for quite some time, a fund like this could be an option.

- Aggressive – Aggressive funds tend to be based on a high-risk, high-return model. You’ll likely see more dramatic changes, but in the long run, you may end up with a lot more of a return.

Financial Acronyms

- Portfolio investment entity (PIE) – A PIE is a scheme or fund that pays tax on its returns based on your Prescribed Investor Rate (see below). Almost every KiwiSaver scheme is a PIE.

- Prescribed investor rate (PIR) – This is the rate at which your returns are taxed when you are in a KiwiSaver scheme that is a PIE (see above). Depending on your circumstances and your taxable income, your PIR could be 10.5%, 17.5% or 28%. It’s important to check that you are on the correct rate to avoid being taxed by default at the highest rate of 28%.

- Member tax credit (MTC) – This is what the government contributes to your KiwiSaver each year. While you’re contributing and eligible, the government puts in 50 cents for every dollar that you contribute up to $521 each year. To receive this top up, you need to put in at least $1042 over the course of the year.

Other investment jargon

- Growth assets – These are usually shares or property and they’re called growth assets because they have more potential to grow in value over time than income assets. These do often involve more risk and will likely have greater ups and downs in value.

- Income assets – Income assets are typically cash or bonds. These kinds of investments receive a regular amount of interest and generally have fewer ups and downs in value than growth assets and involve less risk. They do tend to have lower returns over the long term however.

Still have questions? Get in touch today and we’ll be happy to talk you through it!

KiwiSaver Guide for Employers

Even if you offer a registered superannuation scheme and have an exemption from the Financial Markets Authority, you can’t just ignore KiwiSaver.

As an employer, you must:

- make KiwiSaver available to any staff who want it.

- organise salary deductions for new employees who are KiwiSaver members.

- make employer contributions of at least 3 per cent for employees who are KiwiSaver members.

KiwiSaver for new employees

When you bring on a new employee, you are responsible for checking whether they are eligible to be a KiwiSaver member and if they should be automatically enrolled. You can check their eligibility on the IRD website.

If they aren’t already enrolled

You’ll need to give them a KiwiSaver information pack within 7 days of the employee starting work. This information pack includes a KS2 KiwiSaver deduction form which the employee can use to let you know whether they want member contributions to be deducted at 3%, 4%, 6%, 8%, or 10% of their gross salary or wages. If they don’t advise you of their preferred rate, you should deduct member contributions at the default rate of 3%.

If they are already enrolled

If your new employee is already a KiwiSaver member, they need to give you a completed KS2 KiwiSaver deduction form, and you must deduct member contributions from their first pay, unless you are given a valid savings suspension notice.

A new employee who is an existing KiwiSaver member must:

- tell you their full name and IRD number

- let you know whether they want member contributions deducted at the rate of 3%, 4%, 6%, 8% or 10% or give you a valid savings suspension notice.

KiwiSaver for existing employees

Existing employees aren’t enrolled automatically into KiwiSaver, but they can join as long as they meet the eligibility criteria by contracting directly with their chosen KiwiSaver scheme provider or joining through you as their employer if they are 18 or over.

If an existing employee has told you they’d like to join KiwiSaver, you need to check if they’re eligible and:

- give them a KiwiSaver information pack within seven days

- start making member contributions, at the rate they’ve chosen, from their next pay

- make compulsory employer contributions

- fill out a New Employee KiwiSaver form (IR346K) and send it to the IRD

Employee opt-out request

If a new employee wishes to opt out of KiwiSaver, you need to:

- make sure they’re within the two to eight week opt-out period (on or after day 14 and on or before day 56 of starting employment)

- stop deducting member contributions and making compulsory employer contributions from their next pay

- send both the opt-out and the New employee and KiwiSaver details – IR346K forms to the IRD so they know that the new employee was automatically enrolled and has opted out.

Savings suspensions

KiwiSaver members can take a break from saving 12 months after they’ve made their first contribution to their KiwiSaver – this is called a savings suspension. It can be for a minimum of three months, up to a maximum of one year.

An employee can apply for a savings suspension by calling the IRD, and if approved, either your employee will show you a valid savings suspension notice or the IRD will notify you. You can stop deducting member contributions and making employer contributions once you’ve seen a valid savings suspension notice.

An employee can give you notice that they’d like to restart their deductions but they can’t ask you to start and stop deductions too often; the minimum period before requesting a change is three months.

You aren’t required to pay compulsory employer contributions if an employee is taking a savings suspension, but if you choose to, you can continue to make employer contributions.

Have a question about your KiwiSaver obligations as an employer? Get in touch with our team for more information now.

How to manage your KiwiSaver during tough times

Remember that KiwiSaver is an investment

It can be tempting to switch fund types, decrease your contribution rate, or stop contributing altogether when your balance decreases, but remember that KiwiSaver is an investment, and any changes you make now can affect your retirement down the track. For most people, KiwiSaver is there to be used when they retire so there will likely be many ups and downs before then.

Know your risk profile

Your risk profile is how comfortable you are with different levels of risk or market volatility. If you know you don’t want to take on too much risk, you can align your KiwiSaver fund to suit this. In the same manner, if you know you have a while until you’ll need to access it and you’re fine to ride the waves, you can choose a fund type for that too.

It’s easy to get caught up in the uncertainty and the sometimes ominous-looking market updates, but if you’re going to make changes to your KiwiSaver, make sure you do your research and have realistic expectations.

Don’t lock in your losses

On that note, you might think that switching to a more conservative fund means your KiwiSaver funds will be safer, but this can mean that you’ll likely be locking in your losses and missing out when the market outlook gets brighter again. If you made the decision to be in a certain fund before the market downturn, it will likely still be the right decision for you when things settle down.

Keep contributing if you can

Although many household budgets are feeling the strain right now, it’s important to weigh up the pros and cons of reducing or stopping your KiwiSaver contributions carefully. Any money you keep in your pocket now could mean less when you really need it at retirement.

Plus, every year, the government contributes up to $521 into your KiwiSaver fund if you’ve been contributing regularly over the year. If you stop contributing, you might forget to start again, and you’ll miss out on this great initiative.

Get some support

The balance of your KiwiSaver and whether you should change your fund type might be causing you a lot of undue stress and anxiety. It’s a good idea to chat through your options with an adviser – getting more information can help you feel more in control in deciding how you want to move forward.

Will you get your $521 this year?

What is the Government Contribution?

Every year, the Government makes an annual contribution into your KiwiSaver account as long as you meet the eligibility requirements. For every dollar you contribute (excluding employer contributions) the Government pays 50 cents, up to a maximum payment of $521.43. So to qualify for this extra money, you need to have contributed $1,042.86 throughout the KiwiSaver year (that’s 1 July – 30 June).

Who is eligible to receive this?

Anyone between the ages of 18-65 who lives in New Zealand and is a member of KiwiSaver is eligible to receive this contribution.

You won’t get the full contribution if you turn 18 part-way through the year or if you join KiwiSaver part-way through the year, but you will receive a contribution based on the number of days in the year you’ve been a member.

What if I haven’t contributed $1042.86 throughout the year?

If you haven’t made the full contribution, you will still receive 50 cents for every dollar you did contribute between the 1st of July and 30th June.

To receive the full amount, you can make a voluntary payment to top up your contributions to $1042.86 – as long as it’s received by 30th June, you’ll be eligible for the entire $521.43.

If you’re self-employed and/or are not contributing regularly, it’s a good idea to check your KiwiSaver balance to see how much more you need to contribute to make up $1042.86 before the end of June.

Do I need to do anything?

All you need to do is make sure you’ve contributed at least $1042.86 throughout the KiwiSaver year. If you’re not sure, you can check your balance or ask your KiwiSaver provider.

After the 30th of June, your KiwiSaver provider will apply for the contribution on your behalf. It will automatically be paid into your KiwiSaver account around the end of July, but it could take until the end of August to show up.

If you’d like to look at your options for maximising your KiwiSaver, get in touch with our team of friendly advisers today!

Kids and KiwiSaver

How do I sign my child up?

You’ll need to set them up with an IRD number, you can do this through their website. If your child is under 16, both parents or guardians will need to sign the application form on their behalf. If your child is 16 or 17, they must sign the form alongside their parents or guardians.

What happens if my child starts working?

If your child is under 18 and in paid employment, they can’t join KiwiSaver through their employer, only through a KiwiSaver provider. They’ll need to start making contributions at a minimum of 3% if they get a part-time job, however, you can apply for a savings suspension, for a period between 3-12 months.

Will my child get contributions from the Government or their employer?

If your child is working, their employer isn’t required to contribute to their account until they turn 18, although some may choose to. Government contributions of up to $521.43 a year are available once they turn 18 if they are eligible.

What fees will their account have?

This depends entirely on what provider they are with and what kind of fund they are in. It’s beneficial to do some research on what the providers have available as some of them offer fees-free KiwiSaver accounts for those under 18. Make sure you pick a fund where the fees won’t eat away at their savings.

Can we change their fund later on?

Most definitely! There are a number of different types of funds and providers available to suit each individual. What works for your child now may not work for their goals later down the road. A Haven adviser can provide you with the information you need to decide.

Our advisers are able to provide you with generalised KiwiSaver advice to help you decide what is best for your child’s financial future. If you have any other questions, don’t hesitate to get in touch with our team.

What can you do with your KiwiSaver when you turn 65?

How much can you withdraw?

At 65, you’re able to withdraw all of the money in your KiwiSaver at any time. However, if you choose to withdraw all of your money, you will have to close your account and you’re unable to open another. Some providers can offer you regular automatic withdrawal amounts which might be helpful if you’d like to have a bit of extra cash every week without draining your account. Alternatively, you can withdraw for one-off expenses, like a new car, a holiday or renovations.

Can you still grow your fund?

Choosing to leave all or some of your money in your KiwiSaver account means your fund has the potential to keep growing. If you’re still working, even part-time, you can choose to continue contributing part of your paycheck. If you are planning on leaving your savings in your KiwiSaver account, it’s a good idea to have a chat with a financial adviser to discuss what fund type options are available for you.

Will you still get employer or government contributions?

If you decide to keep working and continue contributing to your KiwiSaver, it’s important to know that your employer is no longer required to match your contributions, however some do choose to continue. You also won’t receive the annual government contribution anymore.

What happens if you die before you turn 65?

If you pass away while your KiwiSaver account is active, the funds will be transferred to your estate. KiwiSaver is considered relationship property so it will be shared with your partner or according to your will. That’s why it’s so important to have a will in place so your money goes where you’d like it to. If you need help, talk to us about getting a will sorted.

If you’re not sure about how to manage your KiwiSaver funds once you’ve turned 65, chat to one of our advisers today.