How much deposit do you need to buy your first home?

- Your deposit size

- Your ability to service debt

Understanding these factors is essential to building a solid foundation for your home-buying journey. Let’s break them down.

How much deposit is enough

Setting a realistic deposit goal is a great starting point. Your deposit size impacts your mortgage eligibility, potential interest rates, and overall loan costs.

Here are some key deposit benchmarks:

- 5% deposit: Minimum required for the Kāinga Ora First Home Loan. It allows you to enter the market sooner but comes with additional costs like Lender’s Mortgage Insurance (LMI) and eligibility criteria.

- 10% deposit: Minimum deposit without government support, low equity premiums (LEP) and low equity margins (LEM) apply.

- 15% deposit: Mid range low equity price point.

- 20% deposit: The ideal target. Reaching this level can unlock the most competitive interest rates and eliminate the need for low equity premium or low equity margin, saving you money over time.

To understand your deposit in context, consider your Loan-to-Value Ratio (LVR). LVR is the percentage of your property’s value that you’re borrowing. For example, if you’re purchasing a home worth $700,000 and have a $140,000 deposit, your LVR would be 80%. Lower LVRs are preferred by lenders because they pose less risk.

Determine your borrowing power

Your ability to service debt is the second factor to consider, and it’s influenced by two key considerations:

- Debt-to-Income Ratio (DTI): This measures how much debt you have relative to your income. A lower DTI improves your borrowing prospects by demonstrating financial stability.

- Monthly cash surplus: This is your uncommitted income after tax minus your living expenses and borrowing repayments (calculated at lender test rates) = your uncommitted income.

Tips to strengthen your borrowing power:

- Reduce personal debt: Lowering debt levels can boost your financial profile.

- Improve your credit score: A strong credit score can qualify you for better loan terms and interest rates. You can boost your credit score by paying your utility bills in a timely manner, avoid overdrawing your accounts or exceeding your credit limit, and ensure any personal finance is paid on time.

- Boost your savings and KiwiSaver contributions: Growing your savings and KiwiSaver contributions not only supports your deposit but also demonstrates solid financial habits to lenders.

- Consider repaying your student loan: Paying off your student loan can positively impact your DTI as you’ll no longer have these deductions from your salary.

- Increase your income: Additional income streams can enhance your borrowing potential.

Next steps: Start planning

Many first-time buyers find they’re closer to their goal than they think! If you’d like help assessing your current position and creating a personalised plan, reach out to us on 0800 700 699 or complete the form below.

*The information contained in this blog is for general information purposes only. It is not intended to constitute financial advice and does not take your individual circumstances and financial situation into account. We encourage you to seek assistance from a trusted financial adviser.

Looking for more support on your home buying journey? Visit our First Home Buyers Guide for helpful resources and step-by-step guidance.

How to grow your first home deposit

Create a budget for your deposit savings

A structured budget is a powerful tool that helps you manage your finances and save effectively for your home deposit.

Evaluate your expenses and prioritise your needs over wants. Cutting back on discretionary spending and redirecting those funds into your deposit savings can make a big difference over time. Following this approach helps ensure you’re consistently saving and keeping your financial plan on track.

To start creating your budget, use the Sorted Budget Planner. It’s a great resource to help you put a plan in place that works for you.

Be purposeful with your budget

A great way to show the bank that you’re financially prepared for a mortgage is to ensure that the total amount you’re saving each month (excluding KiwiSaver contributions) plus your rent payments equals or exceeds what your mortgage repayments would be. This demonstrates to lenders that you can manage the financial commitment of a mortgage and strengthens your application.

Your budget isn’t a restriction but rather a tool to help you understand where your money is going. By using this understanding, you can prioritise your spending to align with your goals.

Strategies to boost your savings

Here are some practical tips:

- Cut non-essential costs: Small changes can add up over time. Consider switching to a cheaper phone or internet plan, buying in bulk, cooking at home instead of dining out, cancelling TV subscriptions, and carpooling or taking public transport.

- Stick to your savings rate: Set up an automatic payment from your account to a high-interest savings account to make savings consistent, and don’t spend it or withdraw it once it’s there!

- Manage debt: Avoid unarranged overdrafts and ensure credit cards are paid off monthly to prevent interest charges. Steer clear of taking on new debt and avoid buy-now-pay-later apps like Afterpay or Laybuy. Watch this video to learn more about managing debt effectively.

- Increase your income: Look for opportunities to boost your earnings by asking for a pay rise, if you haven’t had a recent pay review, back yourself and start the conversation. You could also take on extra work or hours, sell items you no longer need, or rent out a spare room to help cover your current rent or living expenses.

Regularly reviewing and adjusting your budget is key to staying on track. Prioritise your deposit savings and maintain momentum.

Make the most of KiwiSaver

As long as you’ve been contributing to KiwiSaver for at least three years and intend to live in the home for at least the first 6 months, you’re eligible to withdraw all but $1000 of your KiwiSaver savings for your first home. Increasing your KiwiSaver contributions can be an effective way to build your deposit, as it’s automatically deducted from your income before, reducing the temptation to spend.

Next steps

Take time to sit down and develop a detailed budget. Review your current expenses, identify areas for reduction, and allocate as much as possible towards your deposit savings.

If you’re planning to use your KiwiSaver savings for your home purchase, it’s also timely to ensure you’re on track by booking a meeting with a Haven financial adviser. They’ll help make sure your KiwiSaver investment aligns with your goals.

Questions or need assistance? Contact us at 0800 700 699 or complete the form below, and we’ll be happy to help.

*The information contained in this blog is for general information purposes only. It is not intended to constitute financial advice and does not take your individual circumstances and financial situation into account. We encourage you to seek assistance from a trusted financial adviser.

Looking for more support on your home buying journey? Visit our First Home Buyers Guide for helpful resources and step-by-step guidance.

How to access the bank of Mum and Dad

In fact, a recent survey by Kiwibank found that 65% of Gen Z and 43% of millennial home owners have used parental support to purchase their first home.

To help you explore this option, we’ve created a series of videos featuring our Head of Mortgages, Nigel Perkins. In these videos, Nigel breaks down the three most common ways family can help, along with the key considerations and risks for everyone involved.

Gifting

Family Loan

Guarantee

Next steps

If you’re thinking about approaching the Bank of Mum and Dad, it’s important to have a clear plan. Our advisers can help you understand your options and guide you through the process.

Got questions? Call us on 0800 700 699 or complete the form below, we’re here to help.

*The information contained in this blog is for general information purposes only. It is not intended to constitute financial advice and does not take your individual circumstances and financial situation into account. We encourage you to seek assistance from a trusted financial adviser.

Looking for more support on your home buying journey? Visit our First Home Buyers Guide for helpful resources and step-by-step guidance.

How to check in on your home ownership progress

How’s your budget and deposit savings?

Your budget is the foundation of your savings plan, but life happens – sneaky expenses or rising prices can sometimes creep in and throw things off course. Have you noticed any changes to your spending? If so, it might be time to reassess your budget and make small adjustments to keep your savings on track.

Questions to consider:

- Are you consistently meeting your savings targets?

- Are there new expenses you could cut or reduce?

- Have you noticed any price increases that are impacting your progress?

A quick refresh of your budget can make a big difference!

Are you ready for pre-approval?

If your deposit savings are progressing well, it might be time to start thinking about pre-approval. This crucial step gives you a clear idea of how much you can borrow and makes you a stronger buyer when it’s time to make an offer.

Not ready yet? No worries, this is a great opportunity to check in with your Haven mortgage adviser. They can help you identify anything you may need to adjust or prepare to take the next step.

Next steps: Let’s chat

If you’re ready for pre-approval or just want to review your progress, our advisers are here to support you. Whether you have questions about your budget, deposit, or next steps, we’ll guide you through the process.

Call us on 0800 700 699 or complete the form below – we’re happy to help.

Keep going, you’re making great progress, and every step gets you closer to your first home!

*The information contained in this blog is for general information purposes only. It is not intended to constitute financial advice and does not take your individual circumstances and financial situation into account. We encourage you to seek assistance from a trusted financial adviser.

Looking for more support on your home buying journey? Visit our First Home Buyers Guide for helpful resources and step-by-step guidance.

Are you ready for pre-approval? Here’s what to expect

As you continue working towards your goal of home ownership, it’s important to understand what the pre-approval and application process involves. Whether you’re still building your deposit or feeling ready to buy, knowing the steps ahead will help you plan and prepare. You might even be closer than you think!

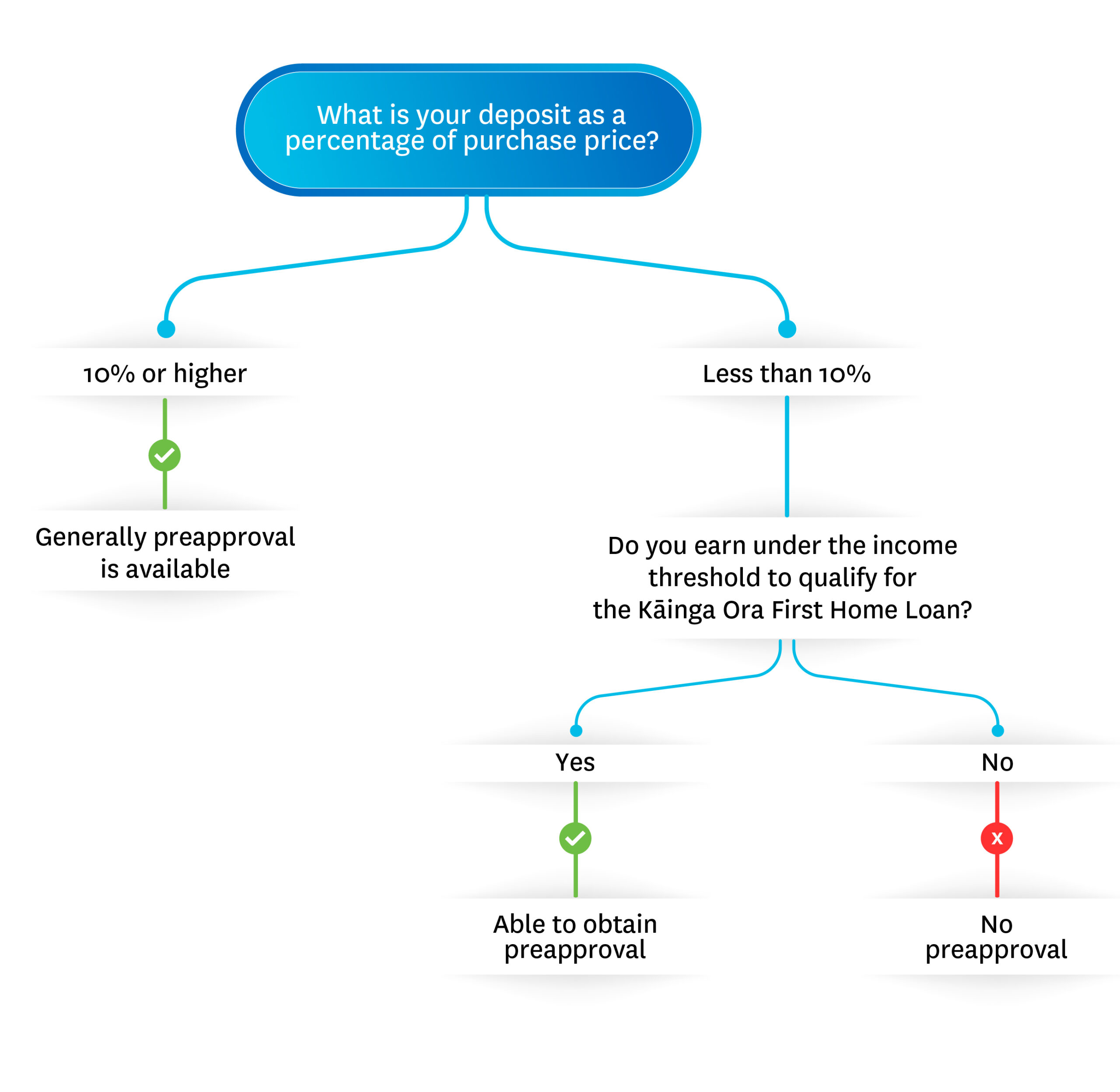

Are you eligible for pre-approval?

An Haven mortgage adviser can help determine whether your current situation meets the criteria for pre-approval. Use the flowchart below as a general guide to assess your eligibility:

You can see the eligibility requirements for the Kāinga Ora First Home Loan here.

If your settings allow you to secure a pre-approval, this makes you more competitive in the property negotiation process. If your settings do not allow you to secure a pre-approval, your Haven mortgage adviser will work with you to navigate the property purchase process, which will likely include a conditional offer.

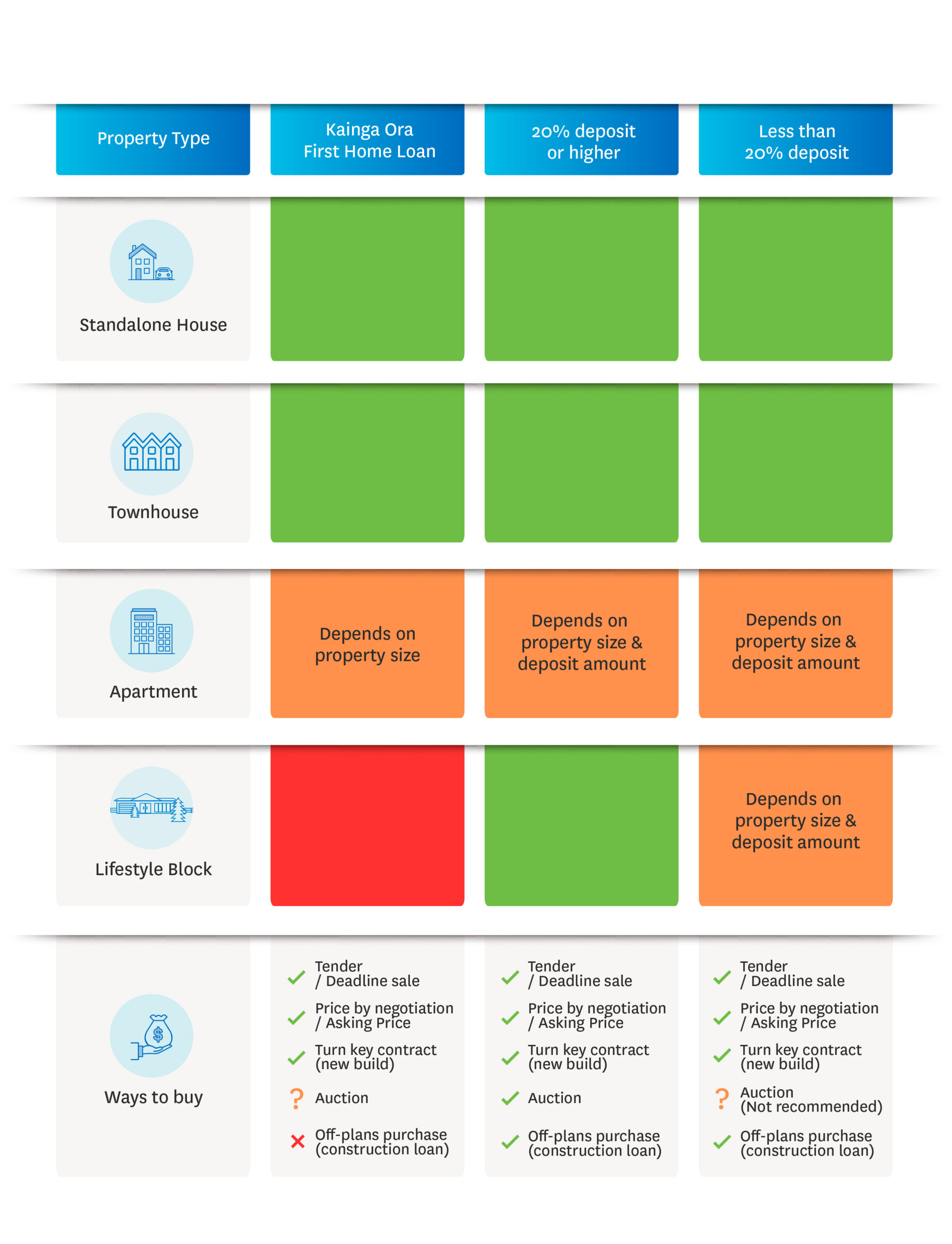

Your settings may also impact the types of properties and purchasing options available. The traffic light guide below outlines the options available, based on your deposit size:

Making an application

When you think you’re ready to submit an application, you’ll need to provide your Haven adviser with a range of documents so they can guide you through the next steps. You’ll need to provide proof of income, proof of deposit, bank statements, statement of financial position (also known as a fact find), and identification.

Once your Haven mortgage adviser has assessed your documents, they’ll let you know if you are ready to submit an application or confirm that you are ready to go house hunting!

Next steps: Initiating your mortgage application

If your Haven mortgage adviser has determined you should progress to an approval (e.g. with a live contract) or a pre-approval, here’s what to expect:

- Connect with your adviser: Your Haven mortgage adviser will advise if you need to provide any further information or documentation and then will submit the application on your behalf.

- Approval timeframe: Expect the approval process to take approximately 1-3 weeks. During this period, banks may request additional documents or information.

- Formal offer: Once approved, you’ll receive a formal letter of offer stating your approved lending amount.

- Pre-approval validity: Most pre-approvals are valid for 3 months, giving you time to find a home that fits your budget. These can often be extended for a further 3 month period if required.

Let’s get started

When you’re ready, send an email to mortgages@haven.co.nz, and we’ll send over all the requirements to get started with your application and how best to send your documents securely.

Haven Mortgages is here to support you through each step of your journey to owning your first home. Don’t hesitate to reach out if you have questions or need assistance.

Questions or need assistance? Contact us at 0800 700 699 or complete the form below, and we’ll be happy to help.

*The information contained in this blog is for general information purposes only. It is not intended to constitute financial advice and does not take your individual circumstances and financial situation into account. We encourage you to seek assistance from a trusted financial adviser.

Your guide to negotiating & settling your first home

Understanding property purchase methods

There are several ways to purchase a property, such as by negotiation, auction, or tender. Each method has its own set of rules and requirements, so it’s important to know which one suits your situation. Auctions, for example, require you to have your financing and due diligence completed beforehand (not recommended for those without pre-approval), while negotiation may give you more flexibility to discuss terms with the seller.

Use our free Haven Property Report

As you explore properties, take advantage of our free Haven Property Report to gain valuable insights into potential homes. The full report provides a comprehensive breakdown of the property details, surrounding area statistics, and an assessed value. To add real weight to your due-diligence on any property, request your Property Report here. Click here to see an example report!

Seek advice

Before making an offer, seek legal advice to ensure you understand the terms and implications of your purchase. Your Haven mortgage adviser can refer you to trusted legal professionals who offer preferential rates for this service.

Additionally, it’s essential to check the insurability of the house for mortgage purposes. At Haven, we work with trusted providers for house insurance, and our advisers can provide guidance on personal insurance cover, ensuring you’re protected and able to meet your mortgage obligations even in case of unexpected health challenges or life events.

You’ll also need to satisfy all your preapproval conditions before going unconditional.

Loan structures and settlements

When it comes to your mortgage, choosing the right loan structure is vital. You may consider fixed rates, floating rates, or a combination of both, depending on your financial situation and goals. Structuring your loan properly can help you manage your repayments effectively and maximise your financial stability. Your Haven mortgage adviser works with you to ensure your mortgage is optimally structured with a key objective to end up mortgage free faster!

Settlement is the final step where the property ownership officially transfers to you. This process includes linking with your solicitor to arrange the payment of any remaining deposit, executing mortgage documents, drawing down your home loan, and receiving the keys to your new home!

Talk to your adviser

Haven Mortgages is here to guide you through every step of the purchase and settlement process. We’re excited to help you take this final step towards owning your first home!

Questions or need assistance? Contact us at 0800 700 699 or complete the form below, and we’ll be happy to help.

*The information contained in this blog is for general information purposes only. It is not intended to constitute financial advice and does not take your individual circumstances and financial situation into account. We encourage you to seek assistance from a trusted financial adviser.

How to manage your mortgage amidst soaring interest rate pressure

Last month we held a webinar led by Nigel Perkins, Head of Haven Mortgages, and joined by legal guru Kelvin Mackie, from Mackie and Co Ltd. The webinar delved into invaluable strategies on navigating the rising market pressures for borrowers and emphasised the importance of proactive engagement when it comes to managing your mortgage. Read on for a summary of the discussion that took place.

The impact of Reserve Bank actions and rising interest rates

Over the past year, the Reserve Bank has responded to inflationary pressures by adjusting the Official Cash Rate (OCR) seven times, raising it from 2.0% to 5.50%. As a result, banks have increased their interest rates from record lows to record highs with best in market 1 year fixed rates surpassing 7% p.a. These changes have added to the financial challenges faced by households.

For more on what rising interest rates really mean for your mortgage repayments, including how to calculate your mortgage repayments using our online mortgage calculator, read our blog here.

Understanding the situation and the unique financial setting of each household

We are seeing more and more clients come to us to talk about their situation with their mortgage repayments, to understand what options are available to them. They want to understand what’s behind the numbers and how we can help them.

Now more than ever, every household should take the proactive stand of facing into their own financial circumstances. Regardless of the size of the mortgage, most households will need to somehow respond to the inflationary led changes and adapt accordingly. Each situation is unique, and it requires careful consideration to identify suitable options.

Exploring mortgage relief options

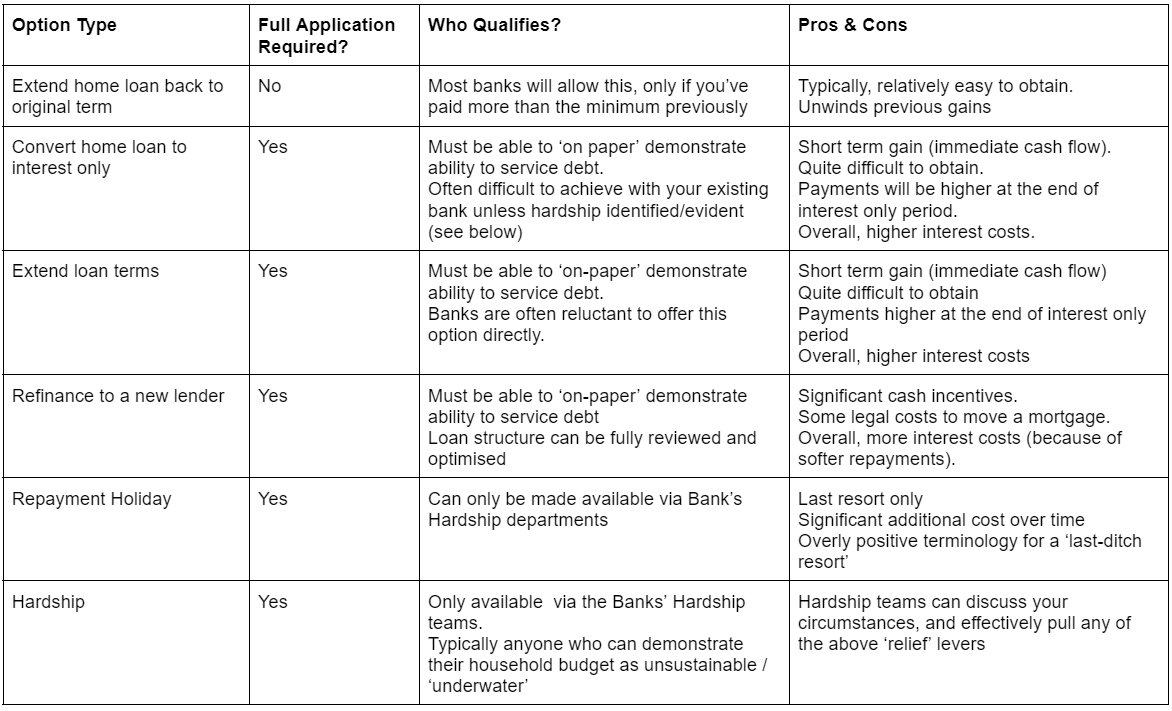

One possible response strategy, is to investigate the merits of softening the impact of interest rate changes. Some households may have the potential to consider and implement some form of mortgage relief. However, if such a plan is contemplated, it’s crucial to understand the associated qualifying thresholds, costs and implications of each option.

The following table outlines some of the possible mortgage relief options that could be made available:

Identifying available options

To identify the best available option to you, first you need to consider where you are at, including understanding your property value, your current lending settings, and your household budget. Get a good lens over what you are trying to achieve and if you’re expecting anything to change in the near future.

From there you can identify what options you may qualify for and whether they are suitable for your current situation. Consider that with a number of the above options you’ll need to show ‘on-paper’ that you can service your debt, for example with refinancing. To do this you’ll need to source a similar degree of information you supplied when you first applied for your loan and prove that you can still service the level of debt, relative to the bank’s servicing thresholds.

Remember that the majority of these ‘relief’ options come at an additional cost over the life of your loan. You should always firstly consider whether any other options are available i.e. reducing household spending elsewhere, and whether your current cash flow really warrants a relief option.

The importance of early engagement and seeking advice

A key takeaway from the webinar was the importance of engaging early to avoid a panic situation. It’s essential to face the reality of the situation as the later it is left the fewer options that will be available to you.

A great place to start is to speak with a Haven Mortgage Adviser to explore your situation and identify what options are available to you to get on top of the situation. Although a mortgage adviser cannot decide for you, they can provide you with their knowledge and education to empower you to make an informed decision.

Bank’s OCR Projections – What they mean and what you can do!

Nigel Perkins, Head of Haven Mortgages, shares his commentary on the Reserve Bank NZ (RBNZ), the Bank’s OCR projections and some key considerations for borrowers.*

RBNZ Commentary

The RBNZ has softened some of its lending ‘speed-limits’ on owner-occupied properties and investment properties. Although these changes aren’t expected to have any material impact on the property or lending market, they signal a softening stance from the RBNZ.

Last month the Reserve Bank announced a further increase in the Official Cash Rate (OCR) to 5.50%. The messaging supporting the increase signalled the top of the interest rate market. Meaning we’re now in ‘hold’ mode, as the RBNZ Governor waits to see whether the economy and inflation pressure responds to the interest rate pressure.

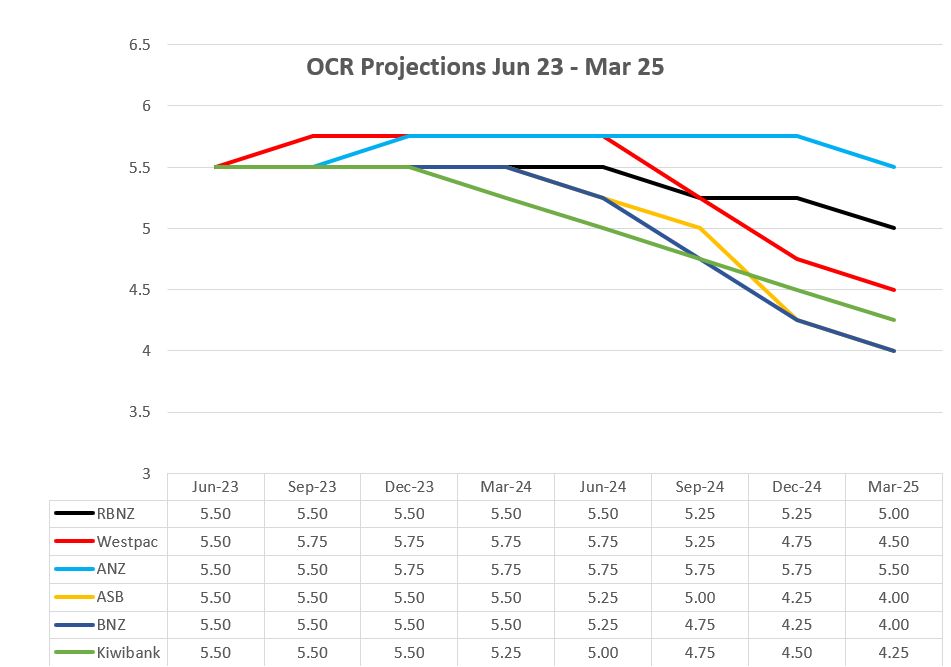

OCR Projections: Overall Banking Lens

Source: Each bank’s website or economic commentary, as at 16/6/23 – some ‘averaging’ may apply if an individual projected quarter was unavailable.

This graph highlights just how variably each bank is projecting progress over the next 2 years, with some quite differing views on the 2 year end position projection, as well as the pathway to get there.

Despite RBNZ’s comments, Westpac are calling for one further OCR hike prior to the election, and ANZ soon-after. Kiwibank, ASB & BNZ are concurring with RBNZ, and are calling the OCR has now peaked, with Kiwibank anticipating the start of the OCR reduction cycle kicking in as early as February ’24.

So, if each of the Bank’s Economics specialists can’t agree on what the future looks like, who do we believe and how do we make a decision on our mortgage? With most of us now facing an inevitable increase in mortgage rates when refixing, what do we do?

ANZ and Westpac’s Economics teams are generally indicating the most overall cost effective refix option is the currently cheaper 3 year fixed option. But there are challenges when locking in for a 3 year term. Although it can mean ‘set and forget’, that strategy has risk, especially if you end up being ‘caught high’ and rates lowering significantly.

Worse, if your circumstances change in say 18 months, and you need to sell – should the market have tracked in line with Kiwibank’s expectations, the OCR and 3 year wholesale rates would have plummeted to or below 4.00%. In light of this, you could then be facing into significant fixed rate break costs.

If the market forces were to dictate the OCR was to start its fall in February ’24, you could assume the 1 year fixed rate was likely also heading south too. On this basis, there could be equally reasonable merit in fixing in for 1 or 2 years now.

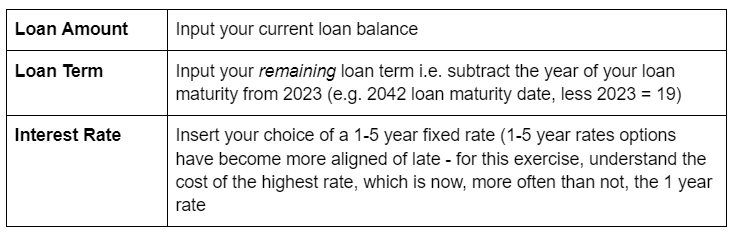

Quick Calculation

To attempt to calculate whether 1 year is better than 2 (in terms of overall, likely costs), you’ll need a few data points and some assumptions. Let’s have a try….

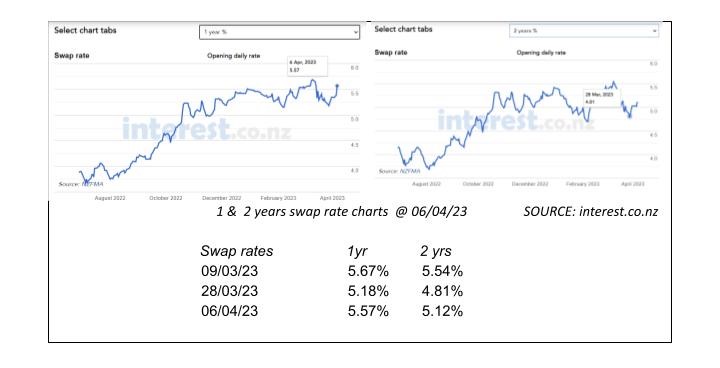

Yesterday (3/7/23) we received some pricing for a $500K refix loan, as follows:

- 1 year fixed 6.79%

- 2 years fixed 6.42%

6.79 – 6.42 = 0.37 differential

For the 1 year rate to be overall more cost effective than the two year rate, the 1 year rate would have to be at least twice the differential rate, in 12 months’ time (being 6.79% – 0.74% = 6.05%).

The question is, do the Banks expect the 1 year rates to be more, or less than 6.05% in 1 year from now? Because the 1 year fixed rates do tend to track in parallel with the OCR movements, you would effectively need the OCR to be approx. 75 bpts lower than today.

Let’s re-check in with their projections, specifically, at the end of June 24:

On these projections, no-one is picking the OCR to have reduced by 0.75% by this time next year. If this proves to be the case, in this scenario, the two year rate offered at 6.42%, appears to be the stronger option.

Do remember, interest rate markets are volatile, and despite all the data available for analysis, no-one gets these projections bang on, consistently. They are merely financial markers, to help inform your overall thinking and decision making.

What should you consider when refixing?

When making fixed rate refix decisions, there are a multitude of factors to consider including (but not limited to):

- What could my new repayments look like and can my household budget withstand it?

- Will I actually need some form of mortgage relief or restructuring?

- Whilst rates are high, am I looking to simply ‘financially survive’ and get by, or am I seeking to continue to fast track my debt reduction?

- Is my intention to pay minimum repayments (i.e. pay the standard ‘contracted’ interest over the loan term) or would I prefer strategies that assist reducing my overall lending as practically and reasonably quickly as possible?

- Do I have any capacity to further reduce debt over the refix period (i.e. any one off windfalls or cash ‘bonuses’?)

- Am I likely to be moving properties during this time?

On the surface, picking a rate and locking it in can be a straightforward administrative exercise. But, picking the right rate and having your loan structure fine tuned to you, your strategies, and your budget… do yourself a service, and roll in the experts at Haven Mortgages. Best of all – they’re free!

*This article does not intend to constitute financial advice and does not take your individual circumstances and financial situation into account.

What do rising interest rates really mean for your mortgage repayments?

Over the past year we’ve heard plenty about increasing inflation and certainly felt the pressure of increasing costs as well. We’ve also seen in the news the Reserve Bank’s attempt to curb inflation with six Official Cash Rate increases since May 2022 rising from 2.00% to 5.25%. This has driven the Banks to increase their lending rates from record lows, to a very challenging current setting, with now best in market 1 year fixed rates nearing 7% p.a.

But all that may have you wondering, what does it really mean for my actual mortgage repayments? Especially if you have a fixed rate expiring, are looking at refinancing or are considering purchasing property soon.

Understanding the potential impacts of increasing interest rates on your mortgage repayments and subsequently your household budget, will help you get prepared now. It will also help you to make an informed decision about any changes you may wish to make to your mortgage going forward.

The tables below show the approximate monthly mortgage repayment on a 30 year term.

So, for example, if a borrower has a $500,000 mortgage with a 4.00% interest rate, their monthly repayments would be around $2,387. If interest rates increase to 7.00%, their monthly repayments would increase to around $3,327. Or, if a borrower has a $1,000,000 mortgage with a 4.00% interest rate, their monthly repayments would be around $4,774. If interest rates increase to 7.00%, their monthly repayments would increase to around $6,653.

Feel free to jump onto our Mortgage Calculator, to see how your new repayments could look, alongside your potential new rates – see latest banks rate here (source interest.co.nz).

Here are our tips for how to calculate your approximate repayments using our Mortgage Calculator:

Tip # 1: When trying to work out what your approximate repayments may look like, following a fixed rate change, insert the following variables via our Mortgage Calculator:

Tip # 2: Bank Economists are generally projecting 1 more OCR rise, to 5.50%, which may push floating and 1 year rates higher still. Longer term fixed rates (less than 2 years) are widely expected to not go higher, and generally now have a future negative bias (source: Westpac Weekly Commentary).

So how can a Haven Mortgage Adviser help?

If you’re worried about paying higher interest rates on your mortgage, a Haven Mortgage Adviser can help you take control of the situation. By quickly reviewing your current and impending financial position and assessing your general affordability profile, all whilst possessing a comprehensive view of the wider market. Amidst all these variables, our team can make recommendations about how you can best manage your mortgage.

Whether through a restructure, refinance or refix there are options to help you get through rising repayments. Contact a Haven Mortgage Adviser today, to take control of your home loan and your budget!

How to manage rising mortgage costs after yet another OCR increase

Nigel Perkins, Head of Mortgages at Haven shares his commentary on the situation and how our advisers can assist you to get in front of it all.

What’s behind the continued Official Cash Rate increase?

Before yesterday’s OCR announcement, the general market sentiment was softening. Market swap rates (used as the yardstick for banks’ 1-5 years fixed rate pricing), were starting to head south, with some market commentary predicting some fixed interest rates had already peaked, even with future OCR increases already priced in.

General sentiment was one or maybe two more OCR increases of 0.25% were likely.

Instead, going against market sentiment, the Reserve Bank announced an increase of 0.5%. Pushing the OCR rate way beyond where the market had expected and reinforcing that inflation and the labour market are out of control. Although in retrospect, the Reserve Bank probably didn’t have much choice.

As an everyday Kiwi, if you hear that interest rates have peaked, you’re more likely to have confidence in your own spending, and you only have to weather a few more dark clouds before the sun is shining again.

‘Confidence’ is the fuel that fires inflation.

Make no mistake, the 0.5% OCR increase announced yesterday, has shut down any such confidence. And, is yet another blow to homeowners and business folk alike.

As the chart below suggests, the impact upon wholesale swap rates is immediate and the trends are the primary drivers of the banking sector’s fixed rate pricing strategy.

Short term rates will likely rise soon i.e., variable rates, through 1 year fixed rates. Interest rate increases sucks a lot of money out of the economy but ultimately, this is what the Reserve Bank needs to truly curb inflation.

If there were only hints of a recession previously, it is now a given. The fall from here will no doubt be hard. Household budgets will be stretched to capacity this year and some, beyond that. This is a cashflow crisis!

What can borrowers do to get in front of it all?

Right now, enquiries from clients are off the chart as people try to understand what sort of mortgage impact pressure is coming and what can be done to navigate it!

Our team can support borrowers to be as proactive as possible, explore if any extreme intervention is needed or if a simple tweak can help you ride out the storm ahead. With a few questions, we can understand your best options and give you confidence going forward.

Options could be:

- Claiming hardship status, and reverting to interest only for a while (when expenses exceed income)

- Restructuring onto softer/longer terms and repayments

- Restructuring onto interest only

- Refinancing to a new banking partner

- Resetting your lending to align to your cashflow

When the property market goes slow, banks pivot and considerable incentives are made available to reward homeowners that shift their mortgage across to them. These incentives are in the form of cash, and are paid instantly upon changing over. Our role is to assess whether this is suitable for you, and if so, maximise the value to you.

So to get in front of it all, make it a priority to get in touch with a Haven Mortgage Adviser today!